Picture this: It’s the beginning of 2020, nightclubs are heaving with people, stores are filled with maskless shoppers and the acronym ‘NFT’ doesn’t exist in modern vocabulary.

How the times have changed. With a seismic shift in the virtual landscape, spurred on by the global pandemic, NFTs have found their way into the mainstream, and these days, everyone from Paris Hilton to Gwyneth Paltrow are talking about Non-Fungible Tokens.

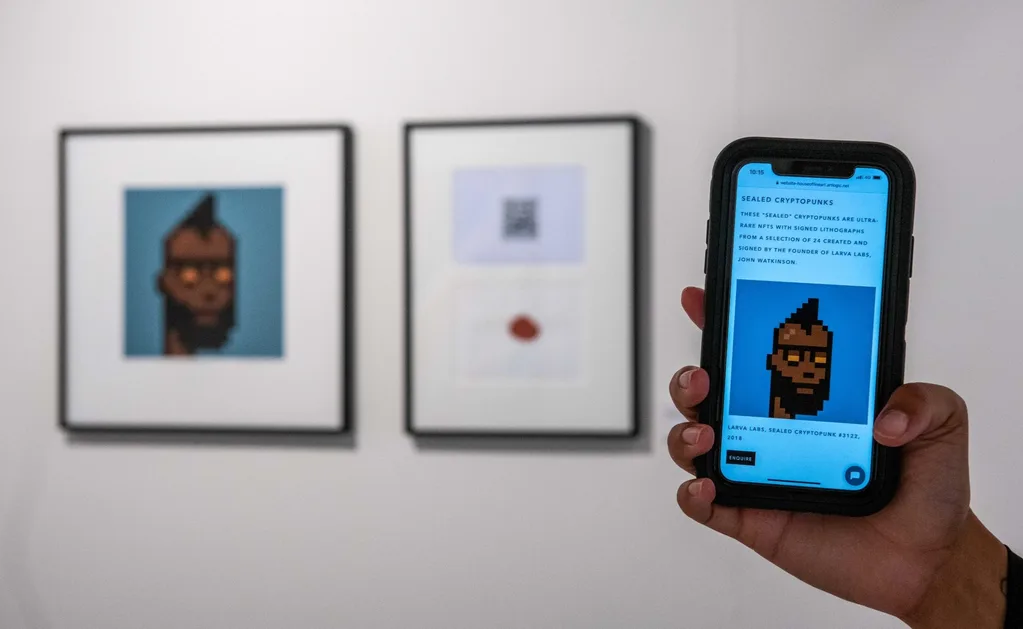

Hilton, who invested in NFT provider Origin Protocol last year and subsequently became a mainstream celebrity face for the craze, is now launching her own collection of NFTs, while Paltrow recently just purchased her own mega-hyped Bored Ape—one of the most popular collections of NFTs out there and an instant status symbol also owned by the likes of Eminem, Jimmy Fallon and Post Malone.

And then there’s the brand hype—Gucci was one of the first major fashion houses to release an NFT, a short film inspired by their ‘Aria’ collection. The four-minute clip sold for USD $25 million (around AUD $34 million).

In September 2021, the Karl Lagerfeld brand released a series of NFTs based on a cartoonish version of the late designer himself. The virtual figurines sold out within 33 seconds.

“People love to show off their prized possessions, we value them more than anything—and the harder to get and rarer they are, the more others want them,” an NFT company co-founder, who asked not to be named, told marie claire Australia. “That’s why some NFTs are skyrocketing in value.”

The NFT market is forecast to reach a value of more than US $35 billion by next year, and $80 billion by 2025.

And with mainstream celebrities and luxury fashion houses—aka the tastemakers and trend-setters of the world—on board, it looks like NFTs are only going to become more mainstream.

But that could be a problem.

The dark side of NFTs

NFTs are largely environmentally unfriendly by design. Marketplaces used to buy and sell them rely on a complex system of puzzles to ensure security, known as ‘proof of work’, which The Verge described as “incredibly energy hungry”. Adding to this is that most NFTs are bought and sold using the cryptocurrency Etheruym, which uses “about as much electricity as the entire country of Libya”.

That said, there are some improvements in the space. Some cryptocurrencies are moving to the ‘proof of stake’ model (as opposed to the ‘proof of work’ model). Here, cryptocurrency holders ‘vote’ on legitimate transactions in order to create new units.

“’Stakers’ are paid in newly created cryptocurrency over time,” Blockchain.com’s head of research Garrick Hileman told Business Insider in December 2021.

“Two major benefits of proof of stake over proof of work are that Proof of Stake can be less energy intensive and have greater transaction throughput (speed) and capacity,” he added.

However, it does come with a disadvantage: “In some systems, you are only selecting validators that have the most money. This means that proof of stake is likely to be significantly less democratic in many cases.”

There’s also the risk that NFTs could be used as tools for money laundering and tax evasion—in a world where a digital art piece can sell for tens of millions of dollars, it’s no surprise (albeit distressing) that some might look to take advantage of it.

It’s also difficult to decipher what a fair market value for any digital piece of art is due to the fact it’s so new—plus, the market itself is volatile. Every day the stock price of Ethereum and Bitcoin goes up and down. In turn, the true worth of an NFT isn’t always black and white.

While we’re yet see any evidence of money launderers invading the space, a Blockchain government affairs analyst told Fortune, “The bad actors are looking for the ways that are most likely for them not to be caught laundering money, and while that’s not to say that it is NFTs, if they find an avenue that they can exploit, they will. They are always probing the fence and looking for the holes.”

To add, buyers run the risk of being scammed or hacked out of their precious goods. Informally coined as ‘The Wild West’, there’s an undertone that the NFT space is anyone’s game, thus, how do we weigh up the positive bragging rights of owning a bored ape against the negatives of an unregulated market, which makes it a playground for scammers?

This seismic shift is not without its risks for major brands, too. Recently, Hermés discovered the market’s complete lack of regulation, when an artist created digital versions of the brand’s highly coveted Birkin bags. The digital bags were reported to cost almost USD $450,000—a price significantly more than your average Birkin.

Hermés launched legal action against the individual, but it’s already a lost battle: each and every MetaBirkin sold has already been placed on the blockchain, and therefore cannot be erased.

When all is said and done, NFTs really are like a prized antique kept locked inside a safe below our beds, only this time, we’re locking them in a virtual space—both are still penetrable, the latter perhaps even more so since it can be accessed by its owner anywhere, anytime.

As for where they’re going is anyone’s guess, it is the Wild West out there after all. Maybe one day, our grandchildren will inherit a pair of virtual sneakers worth 50 times as much as what we once purchased them for. Or maybe one day we’ll look back on the craze, Paris Hilton and all, and remember it as a former hyped-up trend that was simply of its time, its volatility unable to ever overcome its hurdles—as old as the phrase, “That’s hot”.

Lead image: NBC’s The Tonight Show With Jimmy Fallon

Related stories

Native ad body.

Native ad body.

The Aussie Icons the World Can’t get Enough Of

Native ad body.